Do you have an emergency fund? If your answer is no, why not? Many

Americans today still don't have a savings account or an emergency fund. I heard on the news on recently that some Americans

still spend all the money they have. One cause of this is instant gratification. We want everything right now instead of delaying gratification to save up to purchase an item. Nothing remains the same so it's best to be prepared for lean times than to get caught off guard.

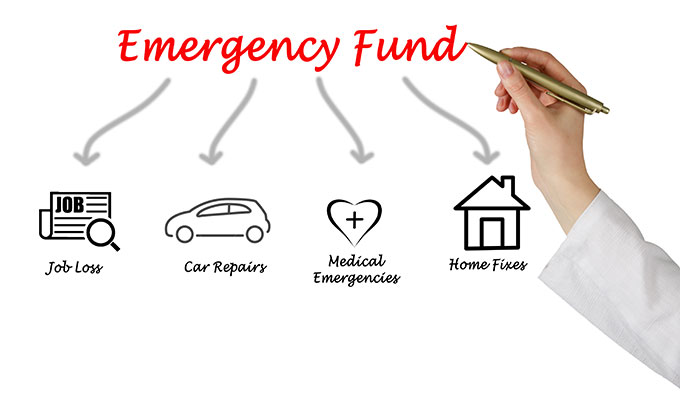

Your emergency fund is a savings account that is used as your safety net –

to help you in case you get sick or lose your job. You can use your emergency fund to hold you

for a few months until you can find a new job or to help you through a financial

crisis. Your emergency fund account

should be separate from you’re your other accounts and should only be used for

emergencies such as an unexpected expense, unemployment, etc.

Your emergency fund money should be easily accessible and stored in a checking

or savings account, preferably a high interest savings account such as Emigrant

Direct, HSBC or ING or in a money market account which allows you to make money

while saving money.

An emergency fund savings account should have enough money to pay your bills for at least 9

to 12 months. To determine how much

money is needed to pay 9 to 12 months worth of your bills do an inventory and

write down all your bills and expenses and the monthly amount spent on each

item. Calculate the total. Use this amount and multiple by 9 or 12 to

determine the total amount you need to save in your emergency fund.

I know what you are saying, I can't even save enough to pay my bills for

one month, how on earth can I start an emergency fund! Start small, even if you save $1.00 a day at

least you are saving and continue to do this until you are able to contribute

more to your savings account.

Once you have saved enough money to pay one bill pat yourself on the back.

Then keep saving until you have enough to pay three bills and so on.

Once you have reached your emergency fund goal then you should start

developing some long-term goals such as planning for retirement. A great site to learn about retirement planning

is www.morningstar.com/Cover/Classroom.html. They provide a great tutorial to

show you the basics of investing. The site also has other great resources on

personal finance, the stock market and other financial topics.

According to the Bureau of

Economic Analysis the current personal savings rate is just a little above 5.5%.

This which means more Americans are paying down debt, planning for retirement

and saving instead of spending.

Don't wait - start your

emergency fund today, it can save your financial life.